When you hear health insurance costs, the total amount you spend on premiums, deductibles, copays, and uncovered medications. Also known as out-of-pocket healthcare spending, it's not just what your employer or the government pays—it's what lands on your bank statement every month. Most people think their monthly premium is the big number, but it's often just the tip of the iceberg. You could have a $200-a-month plan, only to get hit with a $5,000 bill for a single prescription because your drug isn't covered—or your deductible hasn't been met yet.

insurance premiums, the regular payments you make to keep your coverage active. Also known as monthly health plan fees, they vary wildly based on where you live, your age, and whether you get coverage through work or the marketplace. But here’s the catch: a low premium often means a high deductible. That means you pay more upfront before your insurance kicks in. And if you take regular medications—like blood pressure pills, diabetes drugs, or thyroid meds—you could be paying hundreds a month just for your prescriptions, even after insurance. prescription drug coverage, how your plan handles the cost of medications, including tiered pricing, prior authorizations, and step therapy. Also known as formulary restrictions, it’s one of the most confusing parts of health insurance. Two plans might look identical on paper, but one covers your generic version of metformin at $5, while the other makes you pay $85 because it’s on a higher tier. And don’t assume your doctor’s choice is always covered. Many plans force you to try cheaper drugs first—even if they don’t work for you.

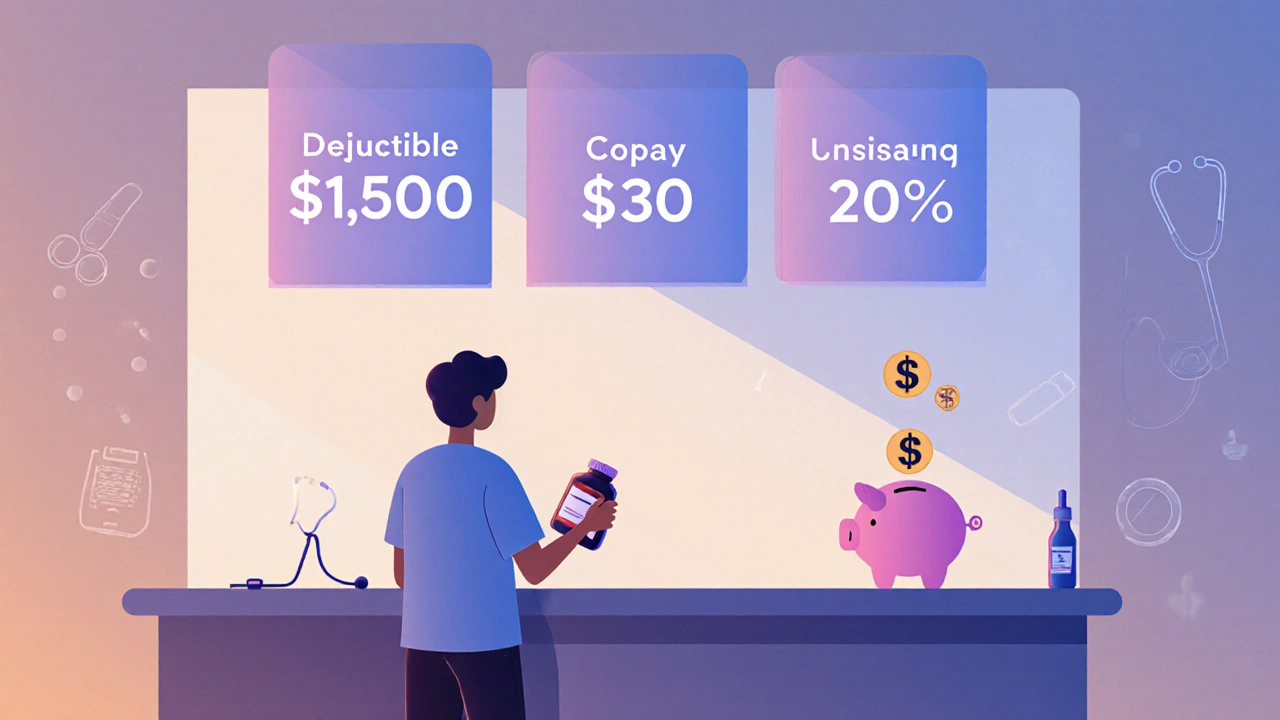

out-of-pocket expenses, all the money you pay directly for care before insurance covers the rest. Also known as medical costs you bear, these include copays for doctor visits, coinsurance for lab tests, and the full price of meds until you hit your out-of-pocket maximum. Some people hit that max in January. Others never do. It depends on your health, your meds, and how your plan is structured. A 2023 study of 12,000 U.S. patients found that 42% skipped or split pills because they couldn’t afford the copay—even with insurance. That’s not rare. It’s routine.

What you’ll find below isn’t theory. It’s real stories and data from people who’ve been burned by hidden fees, surprise bills, and drug pricing games. You’ll read about how the same generic drug costs $3 in Canada and $120 in the U.S., why some insurance plans won’t cover your antibiotic unless you try a cheaper one first, and how a simple blood test can add $600 to your bill because it was done at the wrong facility. You’ll learn how to read your Explanation of Benefits (EOB), how to dispute a denied claim, and where to find lower-cost alternatives for your prescriptions—even if you’re on Medicare or Medicaid.

This isn’t about blaming insurers. It’s about understanding how the system actually works—so you don’t get caught off guard. Because when it comes to health insurance costs, the fine print isn’t just small. It’s deadly.

Learn how deductibles, copays, and coinsurance work in health insurance. Know what you pay for prescriptions and medical care-and how to avoid surprise bills.

View More