When you pick up your prescription or visit the doctor, you might be surprised by how much you have to pay-even if you have health insurance. That’s because most plans don’t cover everything. Instead, you share the cost. This is called cost sharing. It’s not complicated, but it’s often confusing. Deductibles, copays, and coinsurance are the three main ways you pay part of your medical and medication bills. Understanding them can save you hundreds, even thousands, of dollars a year.

What Is a Deductible?

A deductible is the amount you pay out of your own pocket before your insurance starts helping. Think of it like a threshold. Until you hit that number, you cover 100% of eligible costs.For example, if your plan has a $2,000 deductible, you’ll pay the full price for every doctor visit, lab test, or prescription until you’ve spent $2,000 in a year. After that, your insurance kicks in. Some services, like annual checkups or vaccines, are covered for free even before you meet your deductible. That’s thanks to the Affordable Care Act, which requires insurers to cover preventive care without charging you anything.

Deductibles vary widely by plan. Bronze plans often have high deductibles-sometimes $7,000 or more-but lower monthly premiums. Platinum plans have low deductibles, sometimes under $500, but cost much more each month. If you’re healthy and rarely see a doctor, a high-deductible plan might make sense. If you take regular medication or manage a chronic condition, a lower deductible could save you money in the long run.

What Is a Copay?

A copay is a fixed amount you pay at the time of service. It doesn’t change based on how much the service costs. You pay it every time you use a covered service, even if you haven’t met your deductible yet.For instance, your plan might charge a $30 copay for a primary care visit, $50 for a specialist, and $10 for a generic prescription. These amounts are set by your insurance company and listed in your plan documents. Some plans don’t use copays at all-they use coinsurance instead. Others use both: a copay for doctor visits and coinsurance for hospital stays or specialty drugs.

One big advantage of copays is predictability. You know exactly how much you’ll pay each time. No surprises. That’s why many people prefer plans with copays for routine care. But if you need expensive medications, a copay might still feel high. For example, a $75 copay for a monthly insulin prescription adds up to $900 a year-even if the drug costs $1,200. That’s why the Inflation Reduction Act capped insulin at $35 per month for Medicare beneficiaries in 2023. Not everyone qualifies, but it’s a step toward making medications more affordable.

What Is Coinsurance?

Coinsurance is a percentage of the cost you pay after you’ve met your deductible. Unlike a copay, it’s not a fixed amount-it changes depending on how much the service costs.Let’s say your plan has 20% coinsurance. You go to the hospital for a procedure that costs $1,000. Since you’ve already met your deductible, your insurance pays 80% ($800), and you pay 20% ($200). If the same procedure costs $5,000, you pay $1,000 (20% of $5,000). Coinsurance is common for surgeries, imaging tests, and specialty medications.

Many high-cost drugs fall under coinsurance. A cancer treatment that costs $15,000 per month could mean you pay $3,000 if your coinsurance is 20%. That’s why it’s critical to check your plan’s formulary-the list of covered drugs-and how each one is categorized. Some plans put expensive drugs in a higher tier, which means higher coinsurance. Others have separate cost-sharing rules for specialty medications.

How Deductibles, Copays, and Coinsurance Work Together

These three pieces don’t operate in isolation. They stack up in a specific order.First, you pay 100% of costs until you meet your deductible. During this time, you might pay copays for some services (like doctor visits), but for most things-especially prescriptions-you pay full price.

Once you hit your deductible, coinsurance starts. Now you pay a percentage of the cost for covered services. Copays might still apply for certain visits, but they usually don’t count toward your deductible-they count toward your out-of-pocket maximum.

Here’s a real-life example:

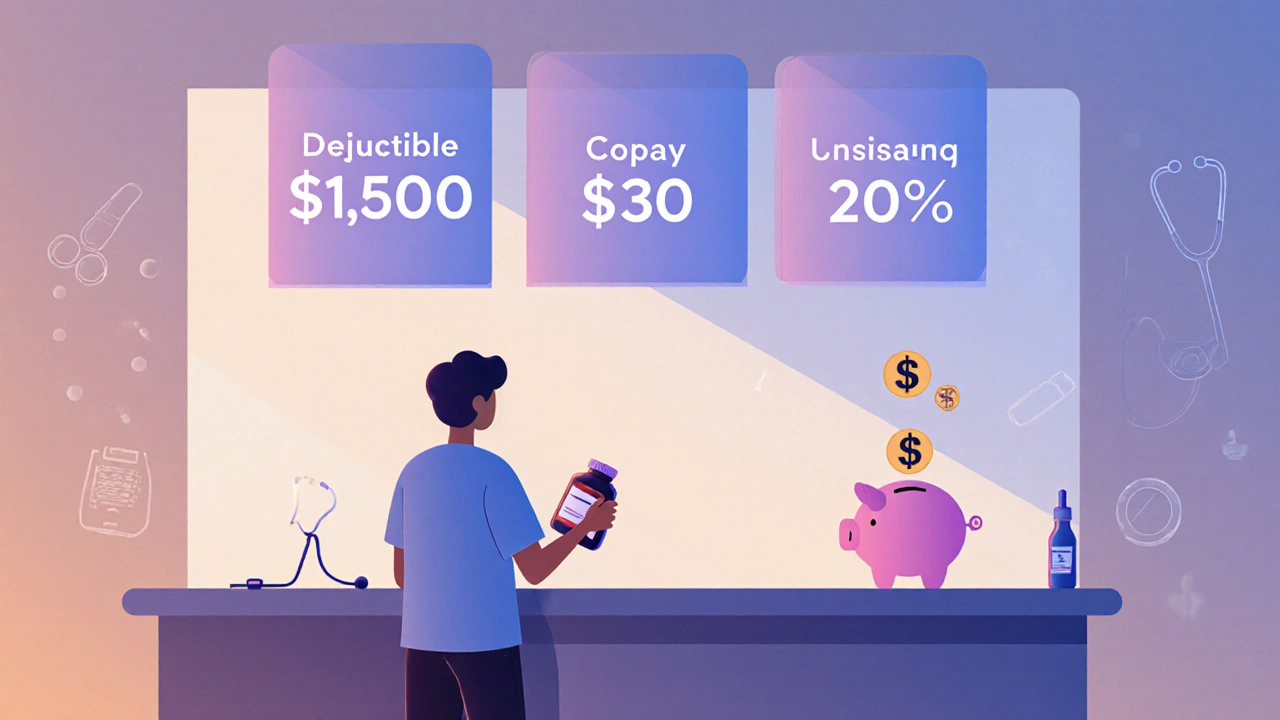

- You have a $1,500 deductible and 20% coinsurance.

- You fill a prescription that costs $120. You pay the full $120 because you haven’t met your deductible yet.

- You visit your doctor for a checkup. Your copay is $30. You pay $30. That doesn’t count toward your deductible, but it does count toward your out-of-pocket maximum.

- Later, you need an MRI that costs $1,000. You’ve already paid $1,500 in total (including the prescription and copays), so you’ve met your deductible. You pay 20% of the MRI: $200.

- By the end of the year, you’ve paid $6,000 out of pocket. Your plan’s out-of-pocket maximum is $7,000. You still have $1,000 left before your insurance pays 100% of everything else.

Out-of-Pocket Maximum: The Safety Net

This is the most important number you need to know. Your out-of-pocket maximum is the most you’ll pay for covered services in a year. Once you hit it, your insurance pays 100% of all covered care for the rest of the year.This includes your deductible, copays, and coinsurance. But it does NOT include your monthly premiums. That’s a common mistake. People think their premium counts toward this limit-it doesn’t.

In 2025, the federal limit for individuals is $9,200 and $18,400 for families. These numbers go up slightly each year. Plans can’t charge more than this, but they can set lower limits.

Why does this matter? If you’re on expensive medication or face a serious illness, the out-of-pocket maximum protects you from financial ruin. Without it, one hospital stay could wipe out your savings. With it, you know exactly how much you’ll pay, no matter how many treatments you need.

How to Avoid Cost Sharing Surprises

Many people get hit with unexpected bills because they didn’t understand their plan. Here’s how to avoid that:- Read your Summary of Benefits and Coverage (SBC). Every insurer must give you this document. It shows real-life examples of how your plan works-like how much you’d pay for a broken arm or a new prescription.

- Check if your pharmacy and doctor are in-network. Out-of-network care often means higher coinsurance or no coverage at all.

- Use your insurer’s cost estimator tool. Most plans have an online calculator that shows estimated costs for procedures and drugs before you get them.

- Ask your pharmacist: “Is this covered under my plan? What’s my copay or coinsurance?”

- Don’t skip preventive care. Annual checkups, cancer screenings, and vaccines are free under the ACA-even if you haven’t met your deductible.

According to the Patient Advocate Foundation, 65% of surprise medical bills could be avoided if people checked their coverage before getting care. That’s not just advice-it’s a money-saving habit.

What’s Changing in 2025?

Health insurance is evolving. More plans are moving toward “value-based insurance design.” That means lower cost sharing for high-value services-like diabetes meds or heart disease treatments-and higher cost sharing for low-value ones, like unnecessary imaging.Also, the Inflation Reduction Act’s insulin cap ($35/month) is now permanent for Medicare. More states are pushing similar rules for private plans. And insurers are being required to show you real-time cost estimates before you fill a prescription.

By 2025, 60% of employer plans are expected to include some form of value-based design, according to McKinsey. That’s good news for people who need ongoing medication. It means your insurance might start helping more-when it matters most.

Bottom Line: Know Your Plan

You don’t need to be a financial expert to understand cost sharing. You just need to know three numbers: your deductible, your copay amounts, and your out-of-pocket maximum. Write them down. Keep them in your phone. Ask questions before you pay.Medication costs are rising. But you’re not powerless. When you understand how your insurance works, you can make smarter choices. You can avoid surprise bills. You can save money. And you can get the care you need without fear of financial shock.

What’s the difference between a deductible and a copay?

A deductible is the total amount you pay each year before your insurance starts sharing costs. A copay is a fixed fee you pay each time you get a service, like a doctor visit or prescription. Copays usually don’t count toward your deductible, but they do count toward your out-of-pocket maximum.

Do copays count toward my deductible?

Usually, no. Most plans treat copays as separate from your deductible. You pay your copay at the time of service, and that amount doesn’t reduce what you owe toward your deductible. But copays do count toward your out-of-pocket maximum, which is the real cap on your yearly costs.

What happens if I don’t meet my deductible?

You pay 100% of the cost for most services until you hit your deductible. That includes prescriptions, lab tests, and specialist visits. But preventive care-like flu shots, mammograms, and annual checkups-is still free, even if you haven’t met your deductible. That’s required by law.

Is coinsurance better than a copay for medications?

It depends. A copay gives you predictability-you always pay the same amount. Coinsurance means your cost changes based on the drug’s price. For expensive medications, coinsurance can be much higher than a flat copay. But for cheaper generics, coinsurance might be lower. Always check your plan’s formulary to see how each drug is priced.

Why do some plans have high deductibles but low premiums?

High-deductible plans keep your monthly premium low because the insurance company is taking on less risk upfront. You pay more when you use care, but less every month. These plans are often paired with Health Savings Accounts (HSAs), which let you save pre-tax money for medical costs. They work well for healthy people who rarely need care-but can be risky if you have chronic conditions or take expensive meds.

Can I be charged for out-of-network care even if I didn’t choose it?

Since January 2022, federal law (the No Surprises Act) protects you from surprise bills for emergency care and certain non-emergency services at in-network hospitals-even if an out-of-network provider was involved. You only pay your in-network cost-sharing amount (deductible, copay, or coinsurance). The rest is between your insurer and the provider.

Next Steps: What to Do Right Now

1. Log in to your insurance portal and find your Summary of Benefits and Coverage. Look for the section on cost sharing. Write down your deductible, copays, and out-of-pocket maximum. 2. Check your most recent prescription. What’s your coinsurance or copay? Is it listed as a tier-3 or specialty drug? That affects your cost. 3. Call your pharmacy and ask: “If I fill this script today, how much will I pay?” Don’t assume-you’ll get the right answer. 4. If you’re on a high-deductible plan and take regular medication, ask if your insurer offers a medication savings program. Many do. 5. Set a reminder for next month: Review your year-to-date out-of-pocket spending. Are you on track to hit your maximum? If so, you might be able to get more care without extra cost.You’re not just paying for insurance-you’re paying for peace of mind. Understanding cost sharing turns confusion into control.

Andrea Jones

November 29, 2025 AT 03:32I get the math. I do. But when you’re choosing between meds and groceries, ‘affordable’ is a luxury word. Thanks for explaining the jargon though. At least now I know I’m not crazy for hating this system.

Justina Maynard

November 29, 2025 AT 09:25Deductibles? More like financial hazing. Coinsurance? A mathematical trap disguised as fairness. And don’t get me started on the 'out-of-pocket maximum'-it’s the only number insurers want you to remember, because it’s the only one that makes them look humane.

Evelyn Salazar Garcia

November 30, 2025 AT 09:23Clay Johnson

December 1, 2025 AT 11:47Jermaine Jordan

December 2, 2025 AT 09:40If you’re reading this and still confused about your insurance-STOP. Right now. Open your portal. Write down your deductible. Call your pharmacy. Do it before your next prescription. This isn’t just money-it’s your health. Your future. Your peace. Don’t wait until you’re in crisis to understand your plan. You owe it to yourself.

Chetan Chauhan

December 3, 2025 AT 20:07Phil Thornton

December 4, 2025 AT 16:49Pranab Daulagupu

December 5, 2025 AT 00:05Alexander Levin

December 5, 2025 AT 11:28Ady Young

December 6, 2025 AT 15:31Travis Freeman

December 8, 2025 AT 09:45Sean Slevin

December 8, 2025 AT 17:10Chris Taylor

December 9, 2025 AT 09:05Melissa Michaels

December 11, 2025 AT 00:59Nathan Brown

December 12, 2025 AT 19:58Matthew Stanford

December 13, 2025 AT 08:56Olivia Currie

December 14, 2025 AT 15:56Curtis Ryan

December 16, 2025 AT 02:36Rajiv Vyas

December 17, 2025 AT 07:09