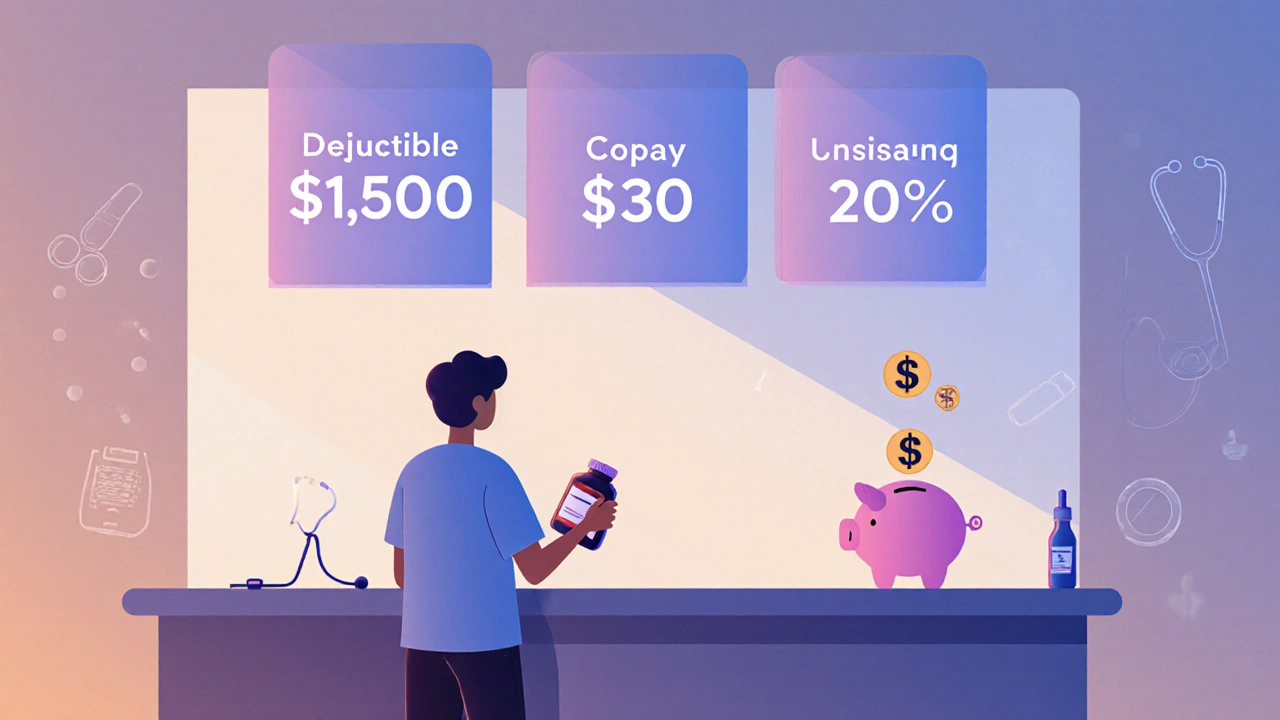

When you hear deductibles, the amount you pay for covered health services before your insurance plan starts to pay. Also known as out-of-pocket thresholds, it’s the first hurdle your insurance makes you clear before it helps cover the cost of your meds. If your plan has a $1,500 deductible, you’re on the hook for the full price of your prescriptions until you’ve spent that much in a year. It doesn’t matter if it’s a $5 generic or a $300 specialty drug—you pay it all until you hit that number.

Not all plans work the same way. Some have separate deductibles for prescriptions, while others combine them with doctor visits and hospital stays. And here’s the catch: even after you meet your deductible, you might still pay coinsurance or copays. That means your health insurance, a contract that pays part of your medical costs in exchange for premiums doesn’t cover everything—even after you’ve paid your share. You could still be paying 20% or 30% of the cost for each refill. That’s why understanding your plan’s structure matters more than just knowing the deductible number.

Prescription costs, the amount you pay out of pocket for medications, including copays, coinsurance, and deductible contributions can swing wildly depending on your plan design. A plan with a low monthly premium might have a sky-high deductible, leaving you stuck paying hundreds for your diabetes or blood pressure meds early in the year. Meanwhile, a higher-premium plan might have a $250 deductible and lower copays—making it cheaper overall if you take multiple prescriptions. It’s not about which plan is cheaper on paper—it’s about which one matches your actual用药 habits.

Many people don’t realize that out-of-pocket expenses, all the money you spend on healthcare before insurance reaches its maximum limit include more than just your deductible. They also cover copays, coinsurance, and sometimes even non-covered drugs. Once you hit your plan’s out-of-pocket maximum, your insurance pays 100% for covered services for the rest of the year. But if you don’t track what you’re spending, you might think you’re covered when you’re not.

What you’ll find in the posts below isn’t theory—it’s real-world insight from people who’ve been burned by surprise bills, saved money by switching plans, or figured out how to time their refills around deductible resets. You’ll see how international drug pricing affects what you pay at the pharmacy, how generic substitution changes your out-of-pocket costs, and why some medications spike in price overnight. You’ll learn how to track your spending, when to ask for a prior authorization, and how to avoid paying full price when you shouldn’t have to. This isn’t about insurance jargon—it’s about making sure you’re not overpaying for the meds you need.

Learn how deductibles, copays, and coinsurance work in health insurance. Know what you pay for prescriptions and medical care-and how to avoid surprise bills.

View More